- Now fully recovered from Covid, cruise passenger numbers are set to grow 5.9% p.a. through 2027

- Financial returns are also improving, thanks to new megaship launches and land investments

- Recent tax concerns interrupted what has been an impressive stock performance: an opportunity?

The clocks having just moved to summertime, no doubt that vacations plans are currently being discussed in many a household, with the booking of a cruise an increasingly popular option. Widely publicised new ship launches, a still low penetration rate, investments in private islands and repaired balance sheets: these are just some of the growth drivers for the cruise industry – as passengers or as investors.

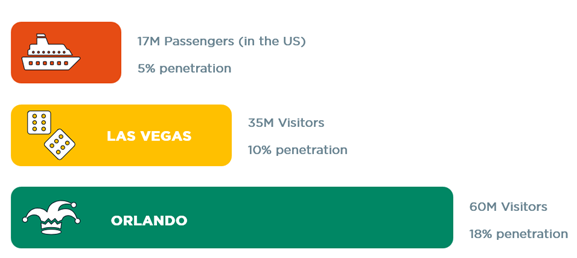

On 27 March, MSC’s newest-built vessel, named World America, left the Saint-Nazaire (France) shipyard for Miami (US), where it will soon be embarking 6,672 guests (and some 2,000 crew members) for luxurious cruises in the Caribbean. Indeed, although passenger growth is now strongest in Asia, Germany and China, North America continues to account for over half (52%) of the global cruise market – and the Caribbean 12% of all cruise destinations.

Looking forward, the number of cruise passengers, which has now well surpassed pre-pandemic levels, is expected to grow 5.9% p.a. through 2027. This thanks to a solid consumer picture but also, and more specifically, a still low penetration level vs. land-based hotels (32 million cruise passengers vs. 2 billion hotel guests) alongside a near 25% price gap. And to dispel the myth of cruising being catered to seniors, note that the average passenger is aged 47-50.

Beyond these favourable macroeconomic drivers, the halo effect from new megaships – such as the MSC World America – serves as a powerful tailwind. Not only do splashy campaigns intensify consumer awareness, as evidenced by the number of cruise searches on internet, but tickets are also sold at a higher price, reflecting the wider range of amenities, and onboard revenues are greater.

Similarly pushing returns up are the land investments made by cruise companies. For passengers, the possibility of spending a day on a privately-owned site, often an island, makes for an easier (and safer) experience than disembarking in a public port. From the cruise operator’s perspective, it enables better control over the guest experience, greater capture of the money spent on land, lower port fees, and can be a means to attract new customers. As of today, 14 such destinations are operational, all in the Caribbean: Carnival boasts a 49% share and Royal Caribbean (with its “Perfect day at CocoCay” offering) is the fast-growing runner-up.

As regards cruise operators’ balance sheets, hard hit by the pandemic, lights are also turning greener thanks to decreasing dependency on agents, portfolio optimisation, a shift from discounting to marketing to fill the ships and longer booking curves.

On the negative side, environmental concerns clearly still plague the industry, notwithstanding progress made in terms of type of fuel used and vessel efficiency. More recently, the bigger worry has been on the tax front though, following comments by the US Secretary of Commerce that the income tax exemptions under which cruise companies work (IRS Section 883) may be amended.

While all cruise company stock prices corrected sharply on this threat, their gains since year-end 2022 are impressive : as of 28 March, Royal Caribbean (the best quality name) is up 323%, Carnival and Norwegian (revival plays) are up 150% and 56%, and Viking (a niche player, offering luxury river cruises) is up 50%, since IPO. Does this mean it is too late to invest? Not in our view. Future waters might not make for plain sailing, but the growth opportunity is real, and valuations not excessive.

Written by Gian Luca Grassini, Junior Portfolio Manager, ESG Analyst

Making the rest of the world great again

- Heightened uncertainties on the back of US policies are clouding a rather supportive backdrop

- A healthy equity rotation, in the same way as freezing temperatures are beneficial to lakes

- Beyond bouts of volatility, there are no compelling catalysts (yet) for a global downturn

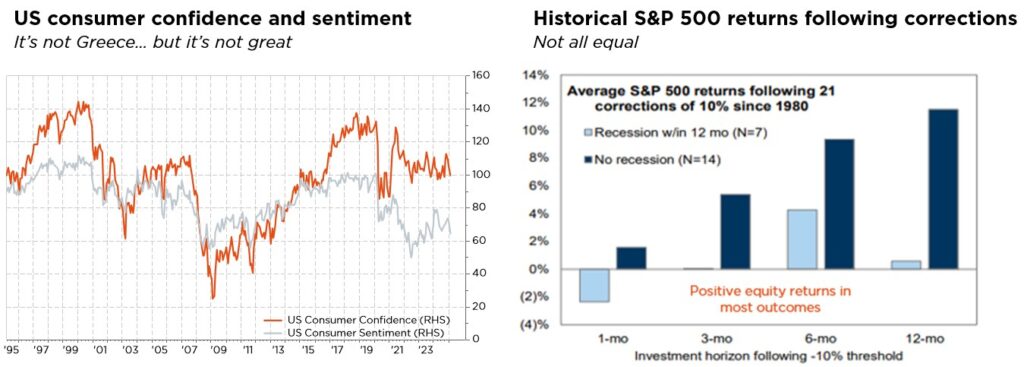

On top of creating uncertainties, Trump policies are also disrupting the world order and leading to historic shifts, with unexpected consequences. It really seems that we are experiencing “…weeks where decades happen”. The good news is that the US administration is putting pressure on the rest of the world and on Europe especially, forcing it to wake up, show off some muscles, regain strength and, as a result, also boosting sentiment in non-US economies and markets. Meanwhile, some cracks have appeared in the resilient US growth narrative and inflation remains like a gum sticking to the Fed’s shoe. Even the “Trump put” has likely been reset lower, with the President seemingly tolerating some temporary downside detox on the US economy and markets in exchange of expected (but very uncertain and thus not guaranteed, in our view) long-term gains. All this has contributed to seriously dent the investor love story with the US exceptionalism fairy tale.

While our central macro scenario remains unchanged (steadily positive growth, sticky but acceptable inflation & gradual rate normalisation in a more divided world), some cautiousness is now warranted given the very uncertain and challenging context brought about by Trump policies and their second-round effects. The next milestone is coming fast, with the April 2nd US tariffs announcement. Downside scenario risks have thus increased somewhat at the expense of our confidence in the central one, while the odds of an upside macro scenario have been kept unchanged thanks to the encouraging signs coming from the rest of the world lately (German fiscal package, improving sentiment in China, ongoing disinflation progress or AI international development).

While on the surface, global equity indices – particularly US ones and even more so their growthier components, such as the Mag7 flagships – did not fare well recently, most regional or sectorial indices have resisted better. Overall, the global equity outlook remains supported by the constructive macro backdrop, alongside resilient corporate earnings (consensus global EPS growth of 11% in 2025), unabated inflows and healthy broader market participation. Furthermore, sentiment has become less greedy, investor positioning is less stretched, US equity valuations have retreated somewhat, dragged down by a 5-10% derating in growth and IT, while our contrarian-indicator is now close to oversold conditions. Put differently, we consider this equity correction as healthy, in the same way as freezing temperatures are beneficial to lakes – mixing surface waters with those at the bottom. As we have flagged many times in the past, stretched valuations are not sufficient per se to prevent positive equity returns, although they may represent a glass ceiling at some point… and turn out as a major headwind when earnings growth peters out (recession) or bond yields surge, which is still not our base case. As a result, we expect equity market gains to track earnings growth and the equity risk premium to contract, if bond yields recede in parallel with eventual disinflation progress. As illustrated lately, elevated equity index multiples conceal a much more complex reality beneath the surface, with segments such as Europe, emerging markets, small- and mid-caps or financials still offering selective pockets of value beyond the magnificent US titans.

At the portfolio level, we maintain a neutral stance on equity and fixed income. This balanced position reflects our assessment of current market conditions and evolving global macroeconomic factors: we are staying invested through a cautiously balanced and well-diversified allocation, which should allow portfolios to benefit from expected positive, but contained, returns in most asset classes this year, while mitigating the bumps and maintaining flexibility to adapt to evolving conditions during the journey. That said, we may opportunistically also add some “cheap” tactical protections to enable the capturing of projected upside potential with a lower risk profile. The other main change to our allocation was a fine-tuning of currency exposure, downgrading our stance on the USD to slight underweight. Indeed, we believe that most of the recent developments and smoke (such as the idea of a Mar-a-Lago Accord) are denting the greenback’s hegemony in the world economic and financial markets.

Written by Fabrizio Quirighetti, CIO, Head of multi-asset and fixed income strategies

External sources include: LSEG Datastream, Bloomberg, FactSet, Goldman Sachs.