Interview with Alexander Roose, Head of Equities and co-lead PM of the DECALIA’s Sustainable strategy

- The properties of hydrogen

- The position of hydrogen in the energy sector

- Market evolution to 2050

- Investment opportunities

In this first ecology series, the focus is on the significant untapped potential of hydrogen. Already more than 5 decades ago, hydrogen made the headlines as the essential fuel source that brought APOLLO crew members to the moon. With the urgency in the EU to lower dependency from Russian gas supplies, on top of the generational challenge to decarbonize our planet, catalysts are finally in place to propel hydrogen adoption in various (new) end markets. For instance, the recently announced REPOWER EU policy contemplates increasing hydrogen usage by more than 20mt. Despite its bright future, in-depth analysis of the hydrogen subtheme (as part of the global Ecology theme) and its value chain are required in order to capitalize on it as an investor. Avoiding the pitfalls and being selective are key, leading us often to below-the-radar investment opportunities.

Why can hydrogen be considered as an attractive energy alternative?

Hydrogen is the lightest and most abundant atomic element in the universe. The extraordinary energy produced by the sun comes from the fusion process of the hydrogen nuclei it contains. This example is enough to demonstrate the properties of hydrogen in terms of an energy carrier which are immense. For the same mass, it concentrates twice as much energy as natural gas and three times as much as oil. But the main attraction of hydrogen today is the contribution it is expected to make to fight global warming. Another key feature is that it does not release carbon dioxide when burned, unlike hydrocarbons. For this reason, it is set to play a key role in the energy transition that is emerging at this historic stage.

In your opinion, which factors are driving the rise of hydrogen in the energy sector today?

There are several catalysts or, if you prefer, several emergencies. Hydrogen today is accompanied by multiple opportunities. It can be used as a fuel to decarbonize several (hard-to-abate) heavy industries, the transportation industry, as a residential heating method or as a solution to store surplus renewable electricity produced by solar or wind power. For these opportunities to become a reality, however, hydrogen must benefit from an economic and policy environment that is strongly supportive. The fact remains that today hydrogen can be said to be on its way to a very positive dynamic. On the longer term, there are the policy measures recently adopted by the European Union. Between the Green Deal, the post-Covid recovery plan focusing on the climate emergency, and the recent REPowerEU plan to reduce dependence on Russian gas, with several initiatives also focusing on the development of green hydrogen, the EU is looking at massively investing in clean and renewable energy.

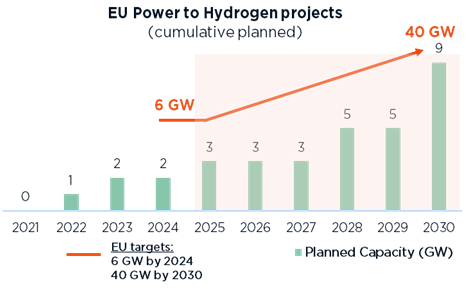

A few figures are enough to illustrate Europe’s ambitions in this direction. By 2050, the EU intends to increase the share of hydrogen in energy production from 2 to 14% and has released the necessary budgets for this. Indeed, the EU foresees allocations of 180 to 470 billion euros for renewable hydrogen and 3 to 18 billion euros for low-carbon hydrogen. These structural policy initiatives have been compounded by the profound impact of the Ukrainian crisis on the energy sector, which has a much tighter time frame to make a lower carbon transition. Europe’s priority is to reduce its energy dependence on Russia, both for gas and oil, as soon as possible. Some countries source up to 40% of their gas from Russia. In this context, it is clear that hydrogen is becoming a particularly attractive alternative, and its deployment is expected to be much faster than predicted last year.

What is the share of hydrogen in the global energy market today?

To date, hydrogen’s share is rather marginal. According to data compiled by the International Energy Agency, global demand for hydrogen in 2020 was around only 90 million tons. This represents barely 2% of all the energy the planet consumes in a year.

How is hydrogen used today?

Mainly in the chemical and oil industries and, to a lesser extent, in the steel industry. These are its main users. The chemical industry alone uses 50 million tons of hydrogen to produce ammonia and methanol. In the oil industry, it is used to remove sulfur in the refining of fuels. And in the steel industry, its ability to burn at very high temperatures makes it an essential agent in the transformation of iron ore into pure steel.

How do you see the hydrogen market developing by 2050?

Over the next two to three decades, the use of hydrogen will increase significantly due to a number of factors that promote its adoption.

For example, that Europe plans to increase the share of hydrogen in its energy production from 2 to 14%. The Hydrogen Council, in collaboration with McKinsey, recently released a report outlining several perspectives for this sector. According to the report’s conclusions, hydrogen could cover one-fifth of the looming global energy needs by 2050.

If we stick to this scenario, this would contribute 20% to the reduction needed to limit global warming by 2° Celsius. The size of the market could approach 2,500 billion dollars and nearly 30 million jobs could be created to support its development.

What are the obstacles that still limit the massive adoption of hydrogen?

Hydrogen has undeniable qualities, but also some drawbacks. Its production process is energy intensive, its distribution is complex to say the least and its adoption cost is therefore quite dissuasive. As for its production, the complications lie in the fact that hydrogen does not exist in its natural state and must therefore be extracted from its atomic formation. To date, 96% of hydrogen is produced from fossil fuels. This is known as gray hydrogen. It is competitively priced, but has the disadvantage of releasing a lot of carbon dioxide during the production process.

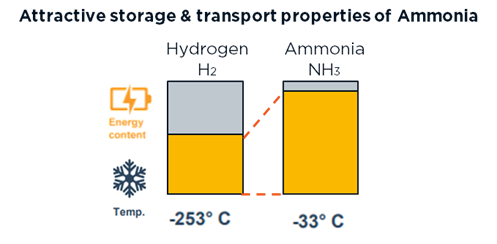

To obtain one kilogram of hydrogen this way, ten times as much CO2 must be released. Therefore, the ideal would be to produce green hydrogen using water electrolysis, with renewable energy as the power source. It is obviously more expensive to produce, but with the surge in EU gas prices and continued decline in LCOE (levelized cost of energy) for solar and wind power , it is starting to become competitive. The other major disadvantage of hydrogen concerns logistical aspects, particularly distribution. To be transported over long distances, it must first be liquefied at very low temperatures, around 250° below zero, and the logistics network required to transport it must therefore meet very challenging technical configurations, with a strong impact on the cost price.

From an investor’s perspective, where do you see the most attractive opportunities?

There are clearly some very good opportunities, but you have to know where to invest in its value chain, since there are many pitfalls or false trails. When we talk about hydrogen, we inevitably think of the transportation sector, electrolysis capacity construction and heating, or industrial fuels.

The Hydrogen Council predicts that between 10 and 15 million cars powered by hydrogen engines will be on the road by 2030. These are projections that are bound to generate a lot of interest. However, it seems to me that the best opportunities at the moment lie elsewhere. This is what emerges from an in-depth analysis of its value chain. In my opinion, the smartest way to capitalize on the hydrogen opportunity today is to consider ammonia producers and industrial gas producers who control the supply chain.

Why is ammonia so relevant to this dynamic?

To some extent, ammonia is paving the way for hydrogen, which has to go through various intermediate stages before it can be fully developed. The same is true for the automotive sector, which had to make a transition to hybrid vehicles before it could really consider all-electricity. The first advantage of ammonia (NH3) is that it contains a large amount of hydrogen. For one molecule of nitrogen, ammonia contains three molecules of hydrogen.

Ammonia is therefore an excellent vehicle for transporting hydrogen over very long distances because, once liquefied, it can be maintained at a temperature of -33° Celsius, far from the -250° Celsius required for hydrogen. Secondly, ammonia is an excellent and widely used chemical (2nd biggest by tonnage) that also has the advantage of not emitting carbon dioxide when used, and is less combustible than gas or hydrogen. It is expected to be first increasingly used as a marine fuel, replacing diesel.

This market is four times larger than that for agricultural ammonia, its traditional usage. Japan is leading the way in this area. There is one final point to mention about ammonia. Its producers have facilities that can be converted to either blue (with carbon capture) or green ammonia. Additionally, the production processes of hydrogen and ammonia share the same technology set-up, be it for gray (steam methane reforming process) or green production (based on electrolysis).

Companies able to manage the supply chain can be considered a good investment opportunity. Could you explain?

Hydrogen has to be stored and transported. This is a key point. There is a lot of value to be created in this logistical control.

Companies such as Air Products, Linde, Air Liquide, OCI and CF Industries are very well positioned in this niche and are therefore expected to play a decisive role in the energy transition.

In Europe, for example, Air Liquide controls more than 50% of the hydrogen (pipeline) supply chain. It already has a turnover of 2 billion euros in the hydrogen sector and its revenues should triple by 2030 because the company is investing heavily in the energy transition. As for CF Industries, based in the United States, the company has the largest integrated ammonia production and distribution network in the world. It will be easy for CF Industries, in the long run, to retrofit its current facilities to capitalise on the hydrogen economy with a clean ammonia product. All of these companies are not yet at the forefront in the minds of investors to capitalize on the hydrogen economy, but they are already well positioned to dominate a market that is set to get bigger and bigger over the next two decades.

About DECALIA Sustainable strategy

- a multi-thematic global equity fund, investing in innovative sectors and disruptive companies shaping our SOCIETY in the future

- invests in the 7 themes (Security, O2 & Ecology, Cloud & Digitalisation, Industrial 5.0, Elder & Well being, Tech Med, Young Generation) regrouped by the acronym SOCIETY

- managed by an experienced team: Alexander Roose (ex-CIO of the Fundamental Equity of Degroof Petercam AM) & Quirien Lemey (ex-Lead PM of a Multi-thematic fund at Degroof Petercam AM)

About DECALIA SA

Established in 2014, DECALIA SA is a Swiss investment management company. With more than 70 employees and assets under management that stand at €4.9 billion, DECALIA has expanded rapidly, in particular thanks to its active-management experience built up over the last 30 years by its founders. The strategies developed by DECALIA focus on four investment themes deemed promising in the long term: the disintermediation of the banking sector, the search for yield, long-term trends and market inefficiencies. DECALIA is regulated by FINMA through a collective assets manager’s license. In addition to its Geneva headquarter, the group has offices in Zurich, Milan & distributors of the DECALIA Sicav in Spain & Germany.