- Recession odds are rising, inflation is taking a backseat and monetary policies balancing act is getting more challenging. These are the consequences of the current banking-stress

- How to position? Don’t overreact but adopt a more defensive positioning by favoring quality and liquidity across the various asset classes

- Cautious tactical stance (Slight Underweight) on both Equities and Bonds, as well as on Gold & Other Commodities, favoring therefore cash.

- Keeping an overall well-diversified equities allocation in terms of geographical, sectorial and style allocation, with a fine-tuning tilt towards defensive sectors, quality style and large cap.

- Favoring US duration and € IG credit on the short end of the curve: US treasuries upgraded to Overweight, while HY is downgraded to Underweight.

- Downside risks to the USD are mounting, especially if a severe global financial crisis is avoided. CHF remains our top pick within currencies.

One year after the first Fed’s rate hike, the aggressive fast monetary policy tightening finally bit… What are the consequences on the overall macroeconomic backdrop from current banking-stress? While their magnitude and extent will obviously depend on the depth of these scars on the financial system, as well as the time to close it, we may nonetheless foresee that:

- Recession odds are rising: growth prospects should be revised lower on the back of tightening financial conditions. Banks will now face higher cost of capital, some liquidity constraints and deteriorating balance sheet quality with economy slowing down, in particular loans related to the US commercial real estate. If credit becomes harder and/or more expensive to get, especially for small and medium companies, which are highly dependent on bank’s loans, it will likely impact negatively investments and hiring prospects.

- Inflation taking a backseat: the inflation issue will certainly move in the background as economic growth will slow faster and sooner than expected, while unemployment rate should start picking up soon too (keep in mind however that labor market is a lagging business cycle indicator).

- Fed bend or break? Major central banks face now a difficult tradeoff between inflation credibility on one side and financial stability and risks to growth on the other side. They decided to proceed with a hike-and-see as inflation has remained uncomfortably high so far, but they also communicated about a more data-dependent path from now. In the meantime, they will continue to provide liquidity, if necessary, to solvent institutions and make sure that the monetary policy transmission to the economy isn’t broken or severely impaired. In this context, additional hikes can’t be ruled out, but we are now closer to the peak. The next ECB and Fed meeting will take place at the beginning of May, letting them sufficient time for a first assessment of the estimated negative impulse to growth and inflation that may eventually lead to a more dovish tactical stance… without abandoning their medium-term objective to bring inflation back to 2%. At this point, it’s worth underlying two major differences between the US and the Europe. First, the European banking sector seems overall healthier than in the US, as US regional banks seems in a particularly precarious situation (less regulation, larger mark-to-market losses on their long duration assets, deposits flight into money market funds, exposure to commercial real estate in the West Coast, …). Then, the ECB remains somewhat behind the curve in its fight against inflation, while inflation may also be stickier, or more structural, in the Euro Area than in the US. In this context, we may expect the ECB would probably sound less dovish than the Fed going forward.

How to position? First of all, don’t overreact! Stay the course of your medium-to-long term investment objectives as history has shown us that sudden changes in risk profile, especially in turbulent times, may be detrimental to wealth over time. In the meantime, we retain our cautious tactical stance (Slight Underweight) on both Equities and Bonds, accounting for positive real rates, higher risk and inflation premiums, geopolitical uncertainties, as well as the relative appeal of cash on the back of its yield & its intrinsic high liquidity feature.

We are thus maintaining our Slight Underweight stance on global equities, via a balanced multi-style all-terrain approach, through a well-diversified allocation in terms of geographical and sectorial allocation given the still remarkably large dispersion of macro outcomes. We have nonetheless fine-tuned our sector & factor preferences this month. More specifically, whereas we adopted a more cautious stance on Banks in the light of recent uncertainties, we have turned more constructive on the high-quality but still unloved Technology sector. Finally, we emphasize our current preference for somewhat safer large cap.

In fixed income, we still favor cash instruments (over bonds) and the short end of the curve globally given the current inverted yield curve shape. As far as duration is concerned, we nonetheless increase it to the upper band of our 3-5 years target range, upgrading US Treasuries to overweight. We prefer US government bonds duration over other sovereign bonds as they will prove the best safe haven if nominal growth peters out and Fed blinks (higher US rates, ECB still behind the curve, EZ inflation more structural, EZ heavy net debt supply this year). Finally, we downgraded HY to underweight as we prefer high-quality fixed income as liquidity support is being removed and growth is slowing. We remain however at ease with IG corporates, especially in the short end of the EUR curve (1-5y) as valuations remain cheaper than in US and companies are usually less leveraged or more diversified in terms of geographical exposure of sales and funding. In other words, similar to equities, we target quality and “large cap” within bonds in order to limit exposure to the most fragile issuers, which will be the first to suffer from deteriorating financial conditions and growth prospects.

Elsewhere, we keep our tactical Slight Underweight on Gold and Other Materials. The precious metal’s upside potential is capped by the Fed’s willingness to restore its inflation-control credibility, while its diversifying effect is being increasingly challenged by a simpler, less volatile and a more yielding alternative… namely cash. We may eventually turn more constructive on gold going forward (and more bearish on the greenback) in case the Fed cut rates sooner and more aggressively than thought. Finally, in currencies, we don’t foresee a major trend for the US dollar in the coming months as long as we remain in this scenario of low but positive global growth without significant divergences in monetary policy trends. However, given the point mentioned here above, we are keeping a slight underweight in USD, which may benefit from a flight to quality effect versus the EUR if banking stress morphed into a more severe financial crisis (not our base case scenario) but it may also depreciate somewhat from now as growth and markets prospects are probably better elsewhere, while Fed is close to peak rates now. In this challenging context, the Swiss Franc remains our preferred currency, supported by still-rock solid structural fundamentals, lower inflation and resilient growth. Here too, quality and defensive features are key.

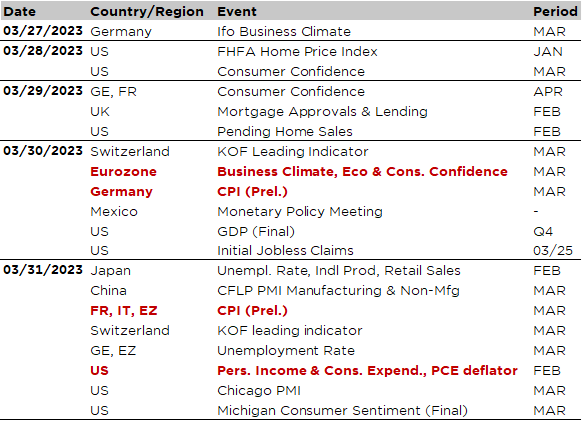

Economic calendar

A lot is going on the markets with investors as well as seasoned economists scratching their heads on the potential impact of baking-stress on growth, inflation and monetary policy trajectories. The banking sector will clearly continue to set the scene this week. However, in terms of economic data, inflation will come back in the forefront as we will get the flash estimates of March inflation in Germany (Thursday) and the Euro area (Friday), as well as the Fed’s favorite inflationary gauge, namely the core PCE deflator, which will be released on Friday afternoon with the February data on US personal income, spending and saving rate.

In the Euro zone, headline annual inflation is expected to decrease further from 8.7% in February to 8.5% this month or lower (preliminary reading), while EZ core inflation should continue creeping up from 5.6% to a new all-time high of 5.8% (or higher) in March. Data for Germany will be out a day before (on Thursday), followed then by reports for the Eurozone, France and Italy on Friday. Looking at the monthly rate of changes, both headline and core inflation are expected to reflect strong gains in excess of +1%, but base effect (more favorable for headline than core index currently), falling commodity prices lately and current robust growth and labor market explain the ongoing divergent trend between headline and core inflation within the euro area.

As far as the US are concerned, the core PCE inflation may show some tentative signs of moderation in February after a surprising acceleration at the start of the year. A monthly reading around +0.3%, will leave the annual core inflation unchanged at 4.7%. With a similar monthly headline inflation of +0.3%, the yoy PCE inflation should drop to 5.1% due to an easy base effect. Higher/lower readings, especially if significantly so, may obviously impact investors’ expectations about future monetary policies, leading then to large swings into bond and equity markets too.

Apart from these inflation figures in Europe and in the US, other noteworthy economic data releases include an array of sentiment indicators for March that will be closely scrutinized to see if there are any potential preliminary impact of the banking turmoil. While most of these indicators should remain broadly unchanged, any unexpected significant declines may add to current markets nervousness

- The German Ifo business climate (today)

- The Conference Board US consumer confidence (tomorrow) and University of Michigan consumer sentiment (Friday)

- The Eurozone business climate, economic and consumer confidence indices (on Thursday)

- The US weekly initial and continuing jobless claims on Thursday to assess “real time” US labor market trend

- China’s PMI manufacturing and services indices (Friday) to assess the speed and magnitude of economic recovery. Current consensus estimates are pointing to a slight deceleration in both indices after the strong rebound, well above 50, of the two prior months.

- The Chicago PMI on Friday

Finally, we will also get some updated data from the Japan economy on Friday with the releases of February unemployment rate, unemployment rate and retail sales. And to conclude with monetary policy, the Bank of Mexico will meet on Thursday and likely hike by +25bps to 11.25%, which could be defined as a very restrictive/hawkish stance when considering that inflation is running now at 7.6% in Mexico after peaking below 9% last summer.

This is a marketing communication issued by DECALIA SA. It is neither directed to, nor intended for distribution or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation. The information and data presented in this document are not to be considered as an offer or invitation to buy or sell any securities or financial instruments nor to subscribe to any services. The information, opinions, estimates, calculations etc. contained in this document reflect a judgment at the original date of publication and are subject to change without notice. Investments in any securities or financial instruments may not be suitable for all recipients and may not be available in all countries. This document has been prepared without taking account of the objectives, financial situation or needs of any particular investor. Before entering into any transaction, investors should consider the suitability of the transaction to individual circumstances and objectives. Any investment or trading or other decision should only be made by the client after a thorough reading of the relevant product term sheet, subscription agreement, information memorandum, prospectus or other offering document relating to the issue of the securities or other financial instruments. Where a document makes reference to a specific research report, the document should not be read in isolation without consulting the full research report, which may be provided upon request.

Unless specifically mentioned, charts are created by DECALIA SA based on FactSet, Bloomberg or Refinitiv data.