•The lifting of Covid restrictions is boosting demand for travel and recreation

•Companies are scrambling to recruit additional workers & having to pay up for them

•Stocks prices are still scarred, making for some interesting but selective opportunities

With summer almost here, the call for the BEACH is growing – as in Booking, Entertainment, Airlines, Cruises & casinos, and Hotels & restaurants. Indeed, the end of lockdowns across much of the globe (China of course excepted) is driving a surge in spending on leisure activities. The demand is such that many companies in these sectors are struggling to ramp up their workforce fast enough, beyond having to cope with high energy prices. An investment opportunity most probably, but one that does require a good dose of selectivity.

Any doubts about the pent-up urge to travel, at least on the consumer side, will have been lifted by the first quarter earnings season. Delta Air Lines reported a return to profitability, earlier than expected, with passenger revenues just 25% short of 2019 levels. Many online travel agents and hotels beat consensus estimates, as did Airbnb. In the cruise segment, Carnival (the largest company and industry proxy) indicated close to 70% ship occupancy in March, vs. 54% for the prior three months. Further positive data points are to be found in visits to internet travel sites, now approaching – in some cases even outdoing – pre-pandemic numbers. And US revenues per available hotel room were up 43% year-on-year for the last week of March, with occupancy improving by 11%: much better than anticipated too.

While not quite as buoyant, business travel is also showing signs of revival, driven by the finance sector and, more latterly, IT and pharmaceuticals. British Airways estimates that professional travellers are now back to 65-70% of the 2019 situation. The problem for the UK airline, as indeed for its US peers, lies in rehiring sufficient workers – after having culled almost 10,000 jobs because of Covid. Pilots have become a scarce commodity! In fact, for lack of personnel, British Airways has been forced to cancel 10% of its scheduled flights for the March to October period.

Yet, investors remain far from convinced. Stock prices in the BEACH* sectors have recouped only part of their Covid losses. In some cases, the market’s caution has to do with financial issues. Cruise companies, for instance, had to raise substantial capital (debt and equity) during the pandemic so as to keep afloat. The greater the investor dilution, the lesser the stock recovery – Royal Caribbean boasting the best performance. More generally, however, investor concerns have to do with macroeconomic risks: higher input costs and a potential economic slowdown.

On the cost side, put simply, it is a story of rising demand meeting constrained supply. Leisure/travel providers are effectively experiencing what goods markets suffered upon the reopening of economies. With rising fuel prices only adding to the burden. In such a context, selectivity is paramount, more so than during the 2020 summer rally. Hotels and restaurants, Compass and Starbucks notably, are probably a safer bet than airlines. In the latter space, one would be wise to prefer a data and transaction processor such as Amadeus IT to the actual carriers. And in entertainment, less impacted by fuel costs, why not consider Live Nation, the global leader in live events?

As for economic worries, they do indeed cast a shadow over the long-term prospects of these cyclical industries, should inflation and higher interest rates bite in too hard on consumer buying power. Come autumn, the ride may well be a bumpy one… But for now, investors headed for the BEACH could enjoy a bumper summer!

*BEACH stands for Booking, Entertainment, Airlines, Cruise & casinos, Hotels & restaurants

Written by Damien Weyermann, Lead PM of DECALIA Dividend Growth

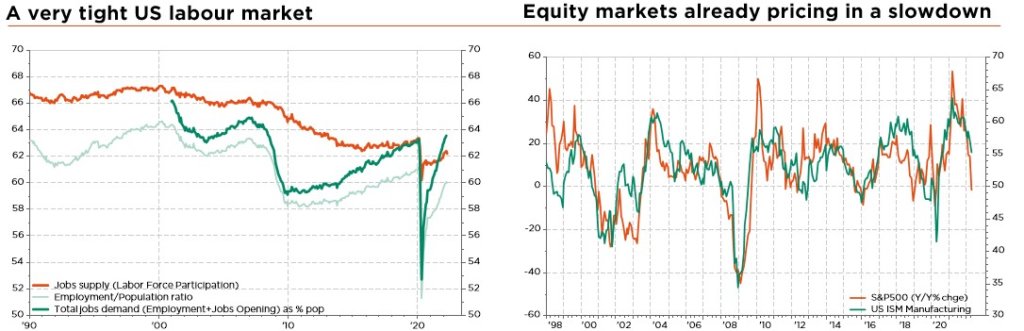

For sure, there are plenty of reasons to be concerned, especially when assessing the overall macro backdrop, which deteriorated further in May. Global economic growth continues to slow, recent inflation data has again tended to surprise on the upside, and the ECB (even SNB) is becoming more hawkish in lockstep with the Fed. Which is why we decided last month to turn more cautious, bringing equities down to a slight underweight.

But while it is easy indeed to look at what is going wrong, some encouraging signs are also appearing. First, despite the many headwinds (rising rates, war in Ukraine, Chinese lockdowns), a recession is not imminent – whereas equity markets are already pricing in a sharp slowdown. Also, inflation is expected to peak this summer: base effects will become more favourable, good prices are already rolling over, supply chain issues will gradually be resolved, and rising rates/slower growth should at some point cap price pressures. Finally, it is hard to see central banks become much more hawkish, at least short term, with markets now pricing in a 2.75% Fed target rate and 0.4% ECB deposit rate by year end.

Turning to the markets, valuations are starting to look attractive, not only on the equity side, with earnings having continued to grow while stock prices nosedived, but also in the fixed income space, where some satisfactory yield can be found, globally, on the short end of the curve. The main concern is that valuations tend to overshoot. In other words, risk-on assets have not yet reached so cheap a level that they become irresistible, regardless of the backdrop or outlook. Pragmatically, this means that currently “risk-light” investors can start to dip a toe in the water, while others should remain somewhat cautious, very selective, well balanced and with a sufficient time horizon.

Financial market pain might not have made enough front pages to resemble prior bottoms, but the good news is that much of the inflation risk, monetary policy tightening and thus rising rates is now priced in, with the collateral effects felt in areas where excessive valuations were the most obvious (thus more prone to a sharp correction) such as unprofitable tech stocks, long-term bonds, or crypto currencies. Moreover, until recently, investors had no choice but to accept equity volatility in the hope of a decent return – on account of the “return-free risk” of bonds, or absolutely no yield on cash. Short-term bonds now provide almost the same yield as longer maturities (with less duration risk), helping mitigate overall portfolio volatility in the current challenging context.

As a result, we are keeping a slight underweight stance on global equities and upgrading bonds to a slight underweight, reflecting an overall cautious and more balanced asset allocation. Within equities, we still favour high quality defensive markets (US and Switzerland) and dividend stocks globally, with the tactical addition of UK exposure, as well as ETFs in natural resources and energy transition in order to adopt a more balanced style positioning. We are also warming up on China, which we had downgraded two months ago, as valuations have become sufficiently cheap and favourable tailwinds are now in sight (end of lockdowns and resumption of easy economic policies).

In fixed income, we are becoming more constructive with valuations clearly improved. The short-end/belly of the curve is now offering some value: we recommend adding to 3-7Y US Treasuries and/or initiating positions on 3-5Y EUR Broad IG, thus keeping duration and credit risk contained.

Elsewhere, we stick to our gold overweight and slight overweight of other materials. Finally, we reiterate our negative tactical view on the EUR vs. USD. Not only are US real rates still more appealing than EUR ones, but the European economy also faces more cyclical and structural headwinds than the US, due to the war in Ukraine.

Written by Fabrizio Quirighetti, CIO & Head of Multi-Asset